By Mark Armbruster, CFA

Now that the presidential election is in the rearview mirror, there is much speculation on what lies ahead for the economy and the stock markets. It is impossible not to let personal politics color your view on this topic, but whichever way you lean, it seems all but certain that the next four years will be defined by disruption.

That disruption could go in a couple of different directions. It could be what economist Joseph Schumpeter called creative destruction. The “you’ve got to break a few eggs to make an omelet” type of disruption that turns out wildly positive in the end. However, there is also a risk that we will have disruption, which is more of the Trumpian chaos we saw in his first administration.

One path could lead to a rebirth of economic growth, while the other could face a long period of stagnation.

The “Renaissance” Scenario

The optimistic view of our coming environment could include an economic renaissance where GDP grows close to 3%, interest rates fall, inflation is finally tamed, and businesses are left alone to drive productivity. Some specific proposals include:

- Cutting corporate income tax rates to 15% and rolling back government regulations.

- Making prior tax cuts permanent and extending tax reductions on certain types of income for individuals.

- Creating the “DOGE” (Department of Government Efficiency) to identify areas of government waste and reduce spending.

Lowering Corporate Tax Rates

If corporate tax rates fall, intuitively, that’s a good thing for corporate profitability. In June 2023, Michael Smolyansky, a Principal Economist of the Federal Reserve, published a study called ‘End of an Era.’ It showed how corporate profits enjoyed a massive tailwind from declining corporate tax rates and declining interest rates for three or four decades.

This study looks at two different time periods: 1962 to 1989, back when tax rates were higher, and 1989 to 2019 when corporate tax rates were falling. If you compare these two periods, the economy grew faster in that earlier period, as the large Baby Boom generation came of age. Corporate sales growth was also higher in the earlier period, reflecting the faster economic growth. However, earnings growth was almost twice as strong in the latter period because the frictions of corporate taxes and interest expense were significantly reduced.

This had a profound impact on the stock market, as the equity risk premium, which is nerdy academic speak for returns in excess of Treasury bonds, was twice as high during the latter period at 7.2% versus 3.6%. Removing obstacles to profitability can be a catalyst for a rising tide that lifts all ships.

Individual Tax Cuts

Trump is also talking about eliminating taxes on Social Security, tip income, and overtime wages. While these should all be stimulative to the economy, we don’t view them all as good policies. One could make the argument that not taxing Social Security makes sense. After all, why does the government give out money and then collect taxes on it? It would be more efficient to just give less money, to begin with. However, favoring certain sources of income from the private sector, like tips and overtime wages, doesn’t make sense to us. Why should the server pay less taxes than someone washing dishes in the kitchen? Nevertheless, more money in the hands of consumers could lead to stronger economic growth.

M&A Activity

The potential for an increase in merger & acquisition deals could also contribute to economic efficiency and further stock market gains. Since the post-Covid pop in activity, both the number and value of deals have declined markedly, to the point that we are back to Obama-era levels.

Trump has promised to remove current Federal Trade Commission Chair Lina Khan, who has been a barrier to closing deals during the Biden administration. When that hurdle goes away, there should be more activity, which could be good for stock market valuations. That is particularly true for smaller-cap stocks because competition among larger potential buyers can help boost their stock prices.

That’s the good news.

The “Lost Decade” Scenario

There is also a lot of uncertainty on the horizon. Instead of having a renaissance we could be heading into a lost decade of low economic growth, high inflation, rising interest rates, and stock market losses. Unfortunately, longer periods of malaise are not unprecedented, particularly from periods of extreme stock market valuation, like today. Proposed policies that could be problematic include:

- Imposing tariffs of 10% globally and up to 60% on goods imported from China.

- Deportation of up to 20 million undocumented immigrants.

- Reducing government spending (which could be good or bad).

Tariffs: Consumers Paying Higher Prices for Goods

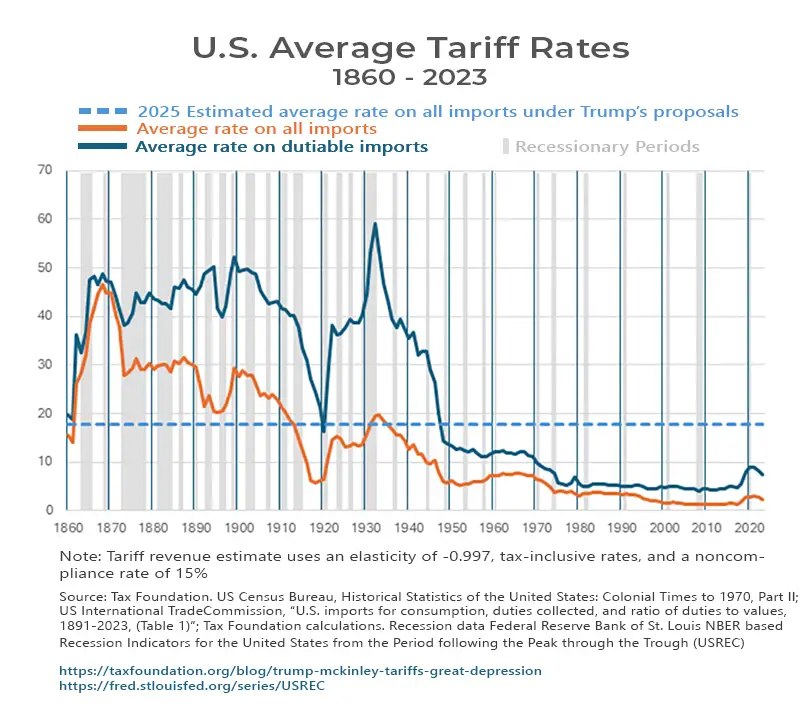

Tariffs are the biggest unknown. They were an important policy tool before the Great Depression in the 1930s. The chart below, which examines historical tariff rates, shows that rates were far higher before 1930 than they are today.

The infamous Smoot-Hawley Tariff Act exacerbated the Great Depression and transformed what might have been a bad recession into a severe, multi-year depression. That is why so many economists are concerned about reinstating a policy tool that could be damaging.

Trump is arguing that tariffs will bring manufacturing back to the U.S. Maybe, but there is evidence that won’t happen, at least on the scale he has discussed. On the other hand, tariffs will certainly raise prices.

It may also be that tariffs are at least partially responsible for the concentrated business cycles that existed before 1930. The gray bars on the Historical Tariff Rates chart represent recessions, and there were a lot more of them before tariffs diminished. Since then, recessions have become less frequent, shorter, and milder, on average, making it easier to weather the storms when they do come. A renewed dependence on tariffs risks taking us back to the prior economic regime.

Immigration and Labor

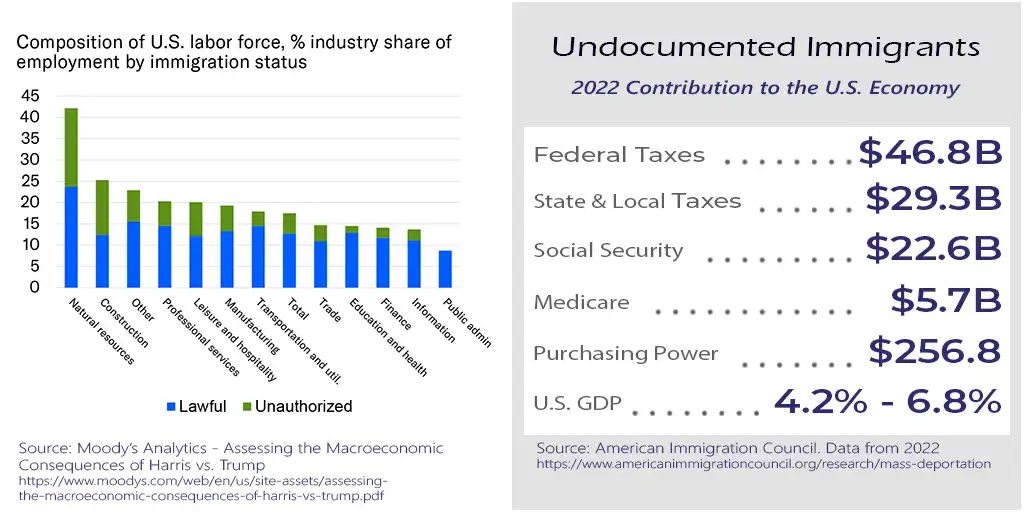

The new administration’s immigration plan could lead to the deportation of millions of undocumented people if fully implemented. Undocumented immigrants make up 20% of the U.S. labor force and generate a sizeable, positive economic impact. They pay taxes and contribute to Social Security and Medicare.

Also, the money they earn results in a lot of purchasing power. In fact, it’s estimated to be 4% to 7% of GDP. So, if these people go away, it will erase all our annual economic growth. The bar chart above, depicting the U.S. labor force composition by immigration status, highlights the potential impact on sectors such as natural resources and construction

Spending Cuts

Cuts to government spending are needed and overdue. The government’s deficit is out of control, and debt-to-GDP is well above sustainable levels. The total annual budget has gone from $118 million in 1965 to $7 trillion in 2024.

The Trump administration, through his DOGE representatives, is talking about cutting $2 trillion from the budget, but it will be tough to identify those savings. 60% of the budget is “mandatory” items like Social Security, Medicare, and Medicaid. 13% is interest on debt that must be paid.

That leaves “only” about $2 trillion that could be cut between discretionary items and defense. However, it seems unlikely Trump would advocate to significantly reduce the defense budget. So, the math doesn’t seem to add up on spending cuts.

The other problem is that even if spending cuts could be identified, it would be highly recessionary to reduce government spending by $2 trillion. Measured against total nominal GDP of $29.3 trillion, $2 trillion comes to 6.8%, which would effectively wipe out nominal GDP, just like deporting all the undocumented immigrants. It is possible that some can be made up by the corporate and consumer sectors, but probably not without a lag and some turmoil that could result in a doozy of a recession.

The Current Environment: Stock Valuations

What does all this mean? Against today’s backdrop with the stock market trading at all-time highs, we’re facing a risky environment ahead.

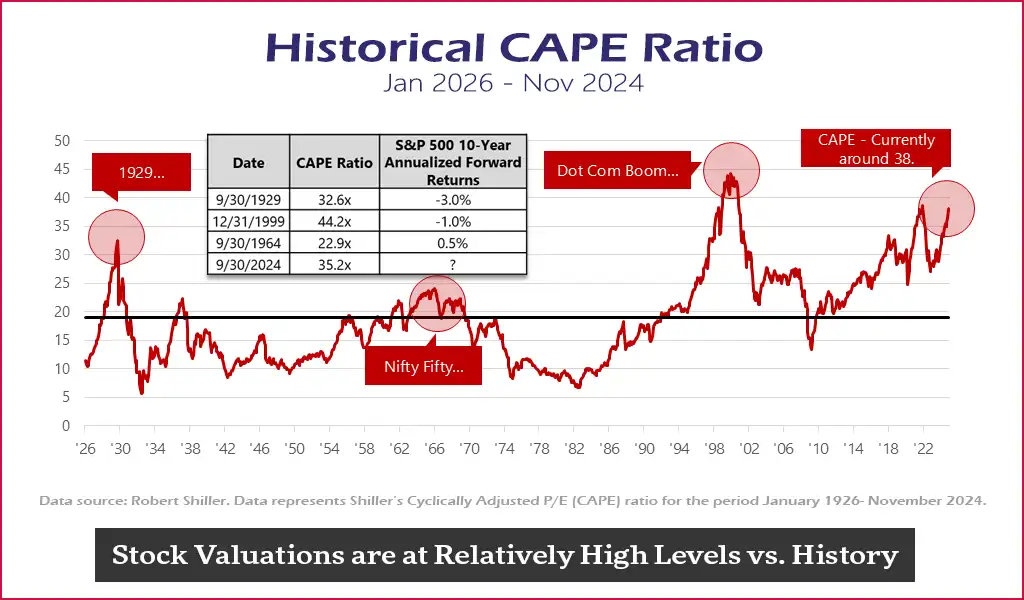

The graph above shows the historical CAPE ratio, a metric developed by Nobel Robert Shiller. It is like the price/earnings ratio but takes today’s stock market price and divides it by the average earnings over the last ten years. The valuation of the overall stock market is the second highest it has ever been, second only to the Dot-Com bubble in the late 1990s. Valuations are even higher than they were just before the Great Depression.

Historically, valuation peaks have preceded periods of flat to down years for stocks. And lost decades have not been unusual. But it’s also not a guarantee that this will recur. CAPE ratios have been above average since the 90s and stock returns have generally fared well.

That said, high valuations do make high future returns more difficult, as incremental gains will be reliant on a continuation of strong earnings growth rather than significant further valuation multiple expansion.

Projected Economic Impact

So, which is it? Are we in a renaissance or a lost decade? The best basis we have for the economic impact of the new administration is probably from forecasts provided by the Penn Wharton Budget Model, Tax Foundation, and the Committee for a Responsible Federal Budget.

They forecast about a half percent drop in GDP from Trump’s policies. Wages could go up minimally, and the deficit could increase by $2 trillion dollars over the next 10 years. Far from solving the debt problem, the experts predict Trump will make it worse. If true, the implications could be significant. There was a study done by economists Reinhart and Rogoff, who looked at the relationship between public debt and economic growth. What they found was that when debt-to-GDP gets above about 90%, there’s a slowdown in future economic growth. That would mean Trump’s proposed policies are detrimental and we’re heading toward the lost decade scenario. But wait.

Bear in mind that the experts are frequently wrong. University of Pennsylvania Professor Philip Tetlock has made a career of studying “the experts,” and hasn’t found them to be very expert. He has noted in his research that the experts don’t seem to have any more insight than anyone else, and in fact, their hubris can often jeopardize their objectivity, resulting in forecasts that are just dead wrong. Another study found that the experts were right 47% of the time, which is worse than a coin flip.

It may also be that we have gridlock, even with the Republicans at the top of the executive branch and in control of both houses of Congress. Not all Republicans are Trump supporters and obstruction would not be surprising.

Unfortunately, all of this doesn’t give us much direction for the year ahead, other than volatility in one direction or the other is likely. There are fancy option strategies one could implement to take advantage of this type of volatility, but probably the best bet is to diversify and focus on the long term.

After all, cycles come and go, and it is best to separate your politics from your portfolio.

For more information on Armbruster Capital’s investment management process and approach, contact us at (585) 381-4180 or info@armbrustercapital.com.

A Tale of Two Economies

By Mark Armbruster, CFA

Now that the presidential election is in the rearview mirror, there is much speculation on what lies ahead for the economy and the stock markets. It is impossible not to let personal politics color your view on this topic, but whichever way you lean, it seems all but certain that the next four years will be defined by disruption.

That disruption could go in a couple of different directions. It could be what economist Joseph Schumpeter called creative destruction. The “you’ve got to break a few eggs to make an omelet” type of disruption that turns out wildly positive in the end. However, there is also a risk that we will have disruption, which is more of the Trumpian chaos we saw in his first administration.

One path could lead to a rebirth of economic growth, while the other could face a long period of stagnation.

The “Renaissance” Scenario

The optimistic view of our coming environment could include an economic renaissance where GDP grows close to 3%, interest rates fall, inflation is finally tamed, and businesses are left alone to drive productivity. Some specific proposals include:

Lowering Corporate Tax Rates

If corporate tax rates fall, intuitively, that’s a good thing for corporate profitability. In June 2023, Michael Smolyansky, a Principal Economist of the Federal Reserve, published a study called ‘End of an Era.’ It showed how corporate profits enjoyed a massive tailwind from declining corporate tax rates and declining interest rates for three or four decades.

This study looks at two different time periods: 1962 to 1989, back when tax rates were higher, and 1989 to 2019 when corporate tax rates were falling. If you compare these two periods, the economy grew faster in that earlier period, as the large Baby Boom generation came of age. Corporate sales growth was also higher in the earlier period, reflecting the faster economic growth. However, earnings growth was almost twice as strong in the latter period because the frictions of corporate taxes and interest expense were significantly reduced.

This had a profound impact on the stock market, as the equity risk premium, which is nerdy academic speak for returns in excess of Treasury bonds, was twice as high during the latter period at 7.2% versus 3.6%. Removing obstacles to profitability can be a catalyst for a rising tide that lifts all ships.

Individual Tax Cuts

Trump is also talking about eliminating taxes on Social Security, tip income, and overtime wages. While these should all be stimulative to the economy, we don’t view them all as good policies. One could make the argument that not taxing Social Security makes sense. After all, why does the government give out money and then collect taxes on it? It would be more efficient to just give less money, to begin with. However, favoring certain sources of income from the private sector, like tips and overtime wages, doesn’t make sense to us. Why should the server pay less taxes than someone washing dishes in the kitchen? Nevertheless, more money in the hands of consumers could lead to stronger economic growth.

M&A Activity

The potential for an increase in merger & acquisition deals could also contribute to economic efficiency and further stock market gains. Since the post-Covid pop in activity, both the number and value of deals have declined markedly, to the point that we are back to Obama-era levels.

Trump has promised to remove current Federal Trade Commission Chair Lina Khan, who has been a barrier to closing deals during the Biden administration. When that hurdle goes away, there should be more activity, which could be good for stock market valuations. That is particularly true for smaller-cap stocks because competition among larger potential buyers can help boost their stock prices.

That’s the good news.

The “Lost Decade” Scenario

There is also a lot of uncertainty on the horizon. Instead of having a renaissance we could be heading into a lost decade of low economic growth, high inflation, rising interest rates, and stock market losses. Unfortunately, longer periods of malaise are not unprecedented, particularly from periods of extreme stock market valuation, like today. Proposed policies that could be problematic include:

Tariffs: Consumers Paying Higher Prices for Goods

Tariffs are the biggest unknown. They were an important policy tool before the Great Depression in the 1930s. The chart below, which examines historical tariff rates, shows that rates were far higher before 1930 than they are today.

The infamous Smoot-Hawley Tariff Act exacerbated the Great Depression and transformed what might have been a bad recession into a severe, multi-year depression. That is why so many economists are concerned about reinstating a policy tool that could be damaging.

Trump is arguing that tariffs will bring manufacturing back to the U.S. Maybe, but there is evidence that won’t happen, at least on the scale he has discussed. On the other hand, tariffs will certainly raise prices.

It may also be that tariffs are at least partially responsible for the concentrated business cycles that existed before 1930. The gray bars on the Historical Tariff Rates chart represent recessions, and there were a lot more of them before tariffs diminished. Since then, recessions have become less frequent, shorter, and milder, on average, making it easier to weather the storms when they do come. A renewed dependence on tariffs risks taking us back to the prior economic regime.

Immigration and Labor

The new administration’s immigration plan could lead to the deportation of millions of undocumented people if fully implemented. Undocumented immigrants make up 20% of the U.S. labor force and generate a sizeable, positive economic impact. They pay taxes and contribute to Social Security and Medicare.

Also, the money they earn results in a lot of purchasing power. In fact, it’s estimated to be 4% to 7% of GDP. So, if these people go away, it will erase all our annual economic growth. The bar chart above, depicting the U.S. labor force composition by immigration status, highlights the potential impact on sectors such as natural resources and construction

Spending Cuts

Cuts to government spending are needed and overdue. The government’s deficit is out of control, and debt-to-GDP is well above sustainable levels. The total annual budget has gone from $118 million in 1965 to $7 trillion in 2024.

The Trump administration, through his DOGE representatives, is talking about cutting $2 trillion from the budget, but it will be tough to identify those savings. 60% of the budget is “mandatory” items like Social Security, Medicare, and Medicaid. 13% is interest on debt that must be paid.

That leaves “only” about $2 trillion that could be cut between discretionary items and defense. However, it seems unlikely Trump would advocate to significantly reduce the defense budget. So, the math doesn’t seem to add up on spending cuts.

The other problem is that even if spending cuts could be identified, it would be highly recessionary to reduce government spending by $2 trillion. Measured against total nominal GDP of $29.3 trillion, $2 trillion comes to 6.8%, which would effectively wipe out nominal GDP, just like deporting all the undocumented immigrants. It is possible that some can be made up by the corporate and consumer sectors, but probably not without a lag and some turmoil that could result in a doozy of a recession.

The Current Environment: Stock Valuations

What does all this mean? Against today’s backdrop with the stock market trading at all-time highs, we’re facing a risky environment ahead.

The graph above shows the historical CAPE ratio, a metric developed by Nobel Robert Shiller. It is like the price/earnings ratio but takes today’s stock market price and divides it by the average earnings over the last ten years. The valuation of the overall stock market is the second highest it has ever been, second only to the Dot-Com bubble in the late 1990s. Valuations are even higher than they were just before the Great Depression.

Historically, valuation peaks have preceded periods of flat to down years for stocks. And lost decades have not been unusual. But it’s also not a guarantee that this will recur. CAPE ratios have been above average since the 90s and stock returns have generally fared well.

That said, high valuations do make high future returns more difficult, as incremental gains will be reliant on a continuation of strong earnings growth rather than significant further valuation multiple expansion.

Projected Economic Impact

So, which is it? Are we in a renaissance or a lost decade? The best basis we have for the economic impact of the new administration is probably from forecasts provided by the Penn Wharton Budget Model, Tax Foundation, and the Committee for a Responsible Federal Budget.

They forecast about a half percent drop in GDP from Trump’s policies. Wages could go up minimally, and the deficit could increase by $2 trillion dollars over the next 10 years. Far from solving the debt problem, the experts predict Trump will make it worse. If true, the implications could be significant. There was a study done by economists Reinhart and Rogoff, who looked at the relationship between public debt and economic growth. What they found was that when debt-to-GDP gets above about 90%, there’s a slowdown in future economic growth. That would mean Trump’s proposed policies are detrimental and we’re heading toward the lost decade scenario. But wait.

Bear in mind that the experts are frequently wrong. University of Pennsylvania Professor Philip Tetlock has made a career of studying “the experts,” and hasn’t found them to be very expert. He has noted in his research that the experts don’t seem to have any more insight than anyone else, and in fact, their hubris can often jeopardize their objectivity, resulting in forecasts that are just dead wrong. Another study found that the experts were right 47% of the time, which is worse than a coin flip.

It may also be that we have gridlock, even with the Republicans at the top of the executive branch and in control of both houses of Congress. Not all Republicans are Trump supporters and obstruction would not be surprising.

Unfortunately, all of this doesn’t give us much direction for the year ahead, other than volatility in one direction or the other is likely. There are fancy option strategies one could implement to take advantage of this type of volatility, but probably the best bet is to diversify and focus on the long term.

After all, cycles come and go, and it is best to separate your politics from your portfolio.

For more information on Armbruster Capital’s investment management process and approach, contact us at (585) 381-4180 or info@armbrustercapital.com.

Share this Article