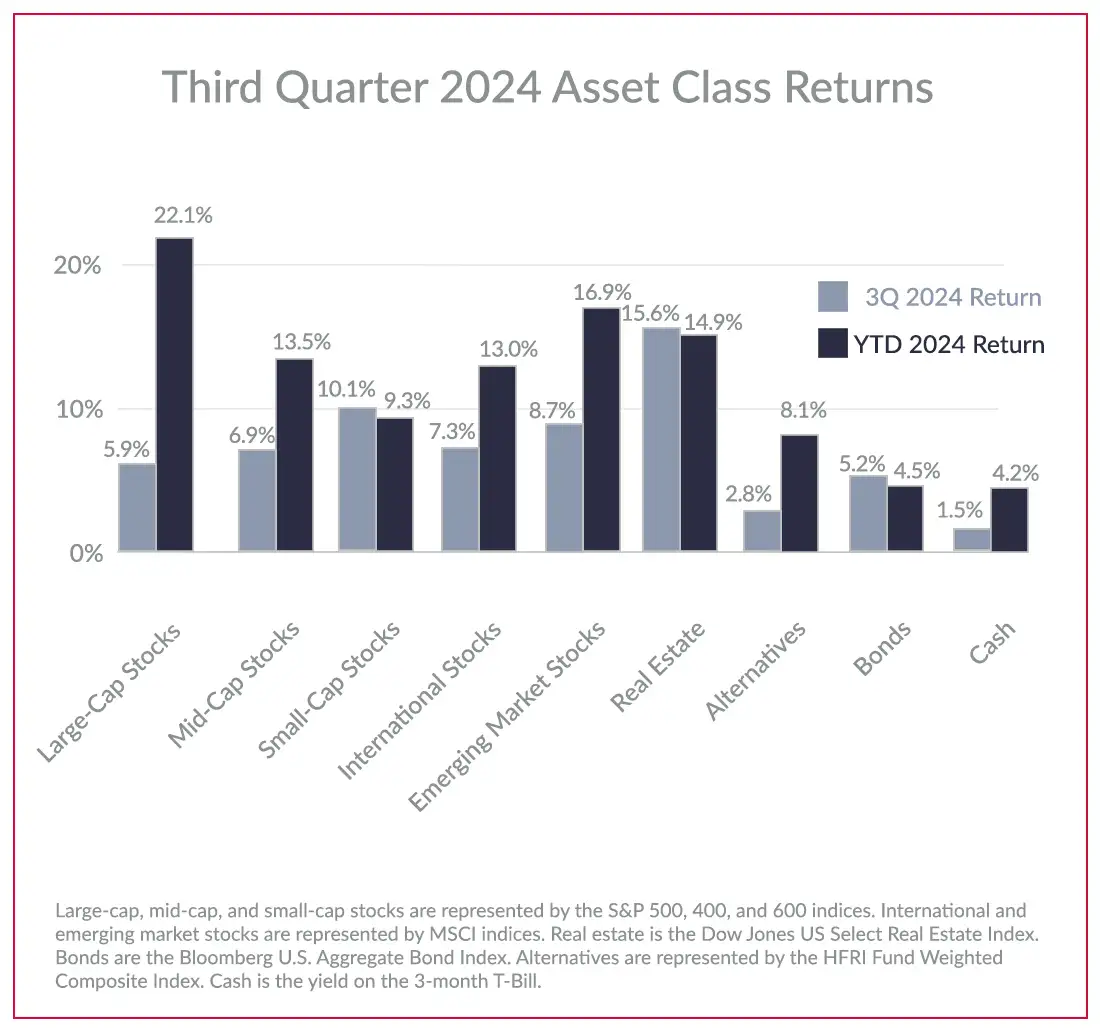

Stock returns were volatile throughout the third quarter, but they did end on a high note and continued to add to their gains for the year. The S&P 500 returned a solid 5.9% for the quarter but mid-cap, small-cap, international, and emerging market stocks performed even better. After posting muted returns during the first half of the year, bonds also had a strong quarter, thanks to a rate cut by the Fed.

CHANGE IN MARKET LEADERSHIP

This quarter saw a welcome change in stock market leadership as small-cap, value, and low-volatility stocks all outperformed the S&P 500. Much of the outperformance for small-cap stocks took place in July when the S&P Small-Cap 600 Index generated an impressive return of 10.8%, almost ten percent greater than the S&P 500 for the month. This can be attributed to softer inflation readings, which bolstered investors’ expectations of a future interest rate cut (that eventually materialized). While a reduction in interest rates is viewed as favorable for stocks across the board, it is especially beneficial for small-cap stocks that often have higher levels of debt relative to their large-cap peers. The same can be generally said for value stocks. Lower interest rates mean higher corporate profits for these firms.

The change in market leadership was also evident among industry sectors in the US stock market. Technology stocks have been on fire for the past several years, but their returns were flat for the third quarter. Energy was the only sector to perform worse, which struggled as oil prices dropped considerably. Meanwhile, real estate, which was the only sector with negative returns in the first half of the year, was one of the best performing sectors in the third quarter. Utilities was another impressive sector, posting a return of nearly 20% for the quarter. The strong performance of this sector can explain why low-volatility stocks did so well, a dramatic and interesting change from technology dominating the market.

Stock Market Asset Class Returns Q3 2024 – Change in Market Leadership

CENTRAL BANK POLICY CHANGES

The change in market leadership that took place throughout most of July was immediately followed by a broad market decline of nearly ten percent. This decline in the first week of August was primarily driven by a combination of weaker than expected economic data releases in the US that increased the likelihood of a near-term recession, coupled with an interest rate hike from the Bank of Japan. The combination of these events caused a mass unwinding of Japanese Yen carry trades, which rattled stock markets around the world. Markets in Japan were especially hit hard, falling 12% in a single day.

However, stocks were able to quickly recoup their losses by the end of the month. US stocks received some additional fuel in September when the Fed cut interest rates by 50 basis points, the first reduction in interest rates since the start of the COVID pandemic. The United States was not alone; China’s central bank also introduced a slate of monetary easing policies to support the nation during its economic slump. Investors responded favorably to these actions, with emerging market stocks soaring to end the quarter.

TREASURY YIELD CURVE NO LONGER INVERTED

The third quarter also marked the normalization of the Treasury yield curve, with the ten-year Treasury yield rising above the two-year Treasury rate for the first time since July of 2022. Historically, an inverted yield curve between ten and two-year Treasury rates has been a reliable recession indicator, preceding every recession since the 1950s. The last few recessions occurred within a year after the normalization of the yield curve and after the first interest rate cut by the Fed, so there is some concern of a near-term recession if history continues to repeat itself.

The cut in the federal funds rate and decline in bond yields has resulted in high returns for bonds for the quarter. The Aggregate Bond Index was up over 5% for the quarter after being slightly negative for the first half of the year.

ALTERNATIVE INVESTMENTS

Liquid alternative strategies were mixed for the quarter. While reinsurance and multi-strategy funds continued their strong performance this quarter, style premia and managed futures strategies took a slight step back. Despite the negative performance of these two strategies this quarter, both still have generated returns of over 15% and 5% year-to-date, respectively. Reinsurance fund returns have been little impacted by damage caused by storms so far this year, but increased risk remains throughout the rest of hurricane season. Regardless, these strategies are meant to be held for the long term to provide meaningful returns that are uncorrelated with stocks. They have been successful in delivering over the last several years.

LOOKING AHEAD

Year-to-date stocks, bonds, and alternative strategies have all provided healthy returns. With the impending election season right around the corner, investors may be concerned as to how the outcome will impact their portfolios. Despite the heightened volatility there may be in the short term, this November we recommend staying the course and keeping a diversified portfolio for the long term.