The stock market fell for a third consecutive quarter, adding to its losses for the year. After a slight rebound to start the quarter, gains reversed sharply in September as the S&P 500 fell by more than 9%, making it the worst month for the index since the Covid downturn of March 2020. International stocks fared worse than domestic stocks this quarter as the strengthening US Dollar continued to pressure returns. The rout in the bond market also extended into the third quarter, with the yield curve elevating to higher levels after two additional 75 basis point rate hikes by the Fed.

PERSISTENT INFLATION

Inflation was yet again a primary driver of weak performance in both stock and bond markets. The Fed remained aggressive in its fight to curb inflation with short- term interest rate hikes and a reduction in the size of its massive bond holdings, which also drains liquidity from the economy. Many countries are currently engaging in similar monetary policies, including the European Central Bank, which raised its rates above 0% for the first time since 2016. Despite efforts globally to reduce inflation, high readings persist. As energy prices eased in June, overall US inflation dropped from its recent high of 9.1%, but it remains at a historically elevated level. Core inflation, which excludes volatile food and energy prices, continued to rise throughout the quarter.

Interest rate hikes by global central banks are meant to deter consumer spending when the economy is overheating. While pent-up demand was the primary driver of inflation in the previous year, it appears to be less of an issue now as indicated by two consecutive quarters of negative real GDP growth. Now it seems supply disruptions are inflation’s primary driver, so monetary policy tools may become less effective (see a further discussion in The Bear Case). In any event, actions by the Fed take some time before their intended effect on inflation is most impactful, so inflation could be around for a while even in the best-case scenario.

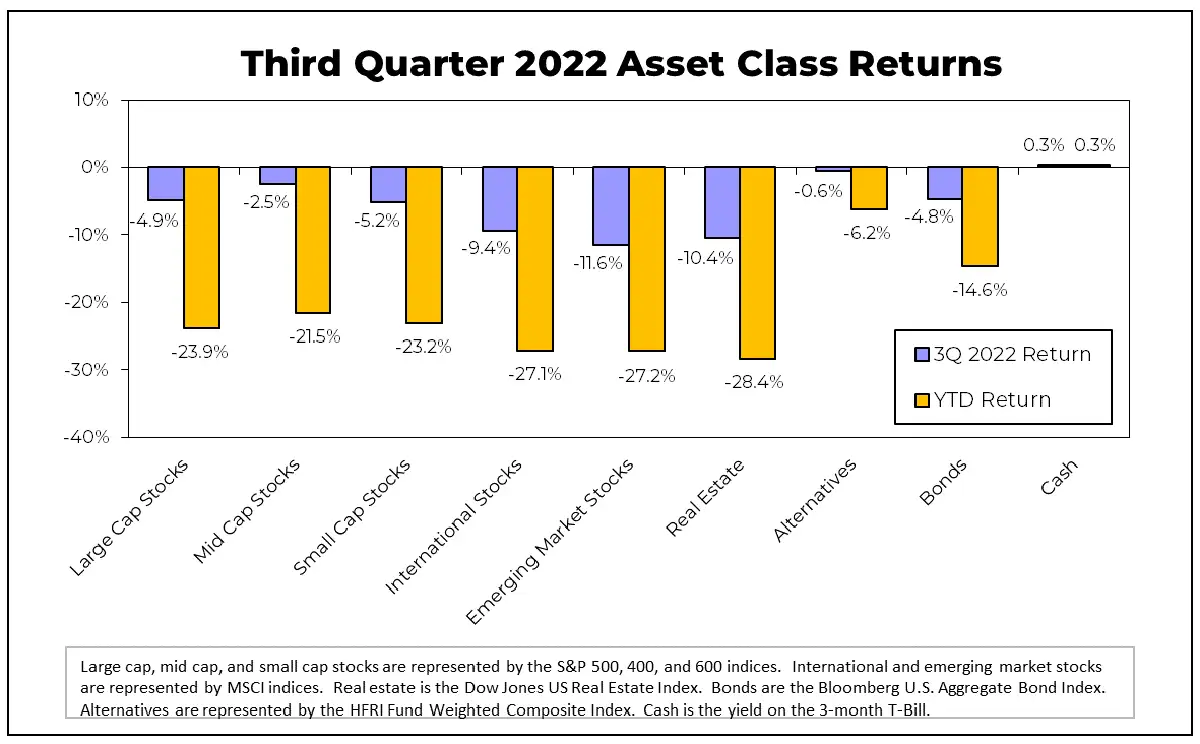

3rd Quarter 2022 Asset Class Returns

EARNINGS FORECAST

Earnings growth for the S&P 500 has come down from its rapid rebound coming out of the pandemic. Inflation’s impact on input costs is a primary reason. While earnings growth is still positive, analysts have been making downward revisions to their earnings estimates for the third quarter and into 2023. Recent movements in economic indicators such as the strengthening of the US Dollar and fall of the ISM Purchasing Managers’ Index are historically correlated with weaker earnings growth. Not surprisingly, recessions often coincide with reduced corporate earnings.

FACTOR AND SECTOR PERFORMANCE

Stock market factors, including segments such as value, momentum, low volatility, and high-quality stocks, trailed overall stock market performance in the third quarter, but are still performing well for the year-to-date period. Large- cap value and low-volatility stocks are both outperforming the S&P 500 by roughly 10% so far this year. Strong performance for the value factor was driven by an overweight in energy stocks and underweight in technology stocks, which were the best and second worst performing sectors year-to- date. A similar dynamic was true for the low-volatility factor, which was overweight utilities and also underweight technology.

VALUATIONS LOOKING MORE ATTRACTIVE

The decline in stock prices has eased valuation ratios that were at historical highs. The CAPE ratio, a measure used to evaluate whether the market is undervalued or overvalued relative to long-term earnings, has fallen from 38 to 28 this year. The trailing twelve-month price/earnings ratio for the S&P 500 is down to around 18, while broad small-cap and international indices have price/earnings ratios in the 10- 11 range, making them historically cheap. Lower starting valuation metrics bode well for higher forward-looking returns. But this is generally true over longer periods and does not mean that there is no more downside in the near-term. Additional downside is certainly plausible, especially considering the potential for a slowdown in corporate earnings.

Even if the market continues to slide, we’ll focus on rebalancing and maintaining long-term diversification, and tax-loss harvesting. These are more powerful strategies than trying to move in and out of the market. For example, investing in the S&P 500 immediately before the Great Financial Crisis of 2007-2009 would have resulted in short-term losses of over 50%. Still, that same ill-timed investment grew at an annualized rate of more than 7% over the next ten years. We understand that market conditions for stocks and bonds this year have been painful but staying the course during turbulent times has proven beneficial in the long run.