The first half of 2022 has been challenging for both stock and bond investors as persistently high inflation, anticipation of further Fed interest rate hikes, and negative GDP growth weighed on returns. The S&P 500 experienced its worst first half of the year since 1970, while bonds have experienced a loss of more than 10%.

INFLATION CONTINUES TO RISE

Concerns over inflation that hampered first quarter returns escalated in the second quarter as CPI continued to increase to a high of 8.6%. With inflation appearing to be less transitory than previously anticipated, the Fed took more aggressive actions in its latest meeting by raising the Federal Funds rate by 75-basis points, the first time it has done so since 1994. Additional restrictive monetary policy measures, such as further rate hikes and reducing the Fed’s balance sheet are likely needed to tame inflation, especially when considering that the Federal Funds rate is still notably below the current inflation rate and the Fed’s balance sheet has continued to grow since the beginning of the year.

Energy stocks remain the winning sector so far this year thanks to elevated oil and gas prices. Energy has been the only sector delivering positive returns this year and is up more than 30%. Despite its strong performance recently, the energy sector still has the second lowest price-to-earnings ratio, with only financial services being lower. Non-cyclical sectors such as utilities and consumer staples are also holding up much better than the rest of the market as they are down only -0.6% and -5.3% this year, respectively.

Low volatility and value have been the strongest performing factors for both US and international stocks. Low volatility has a high allocation to non-cyclical industries that tend to hold up better during challenging environments. Value has done well with its tilt towards energy stocks as well as its avoidance of many overvalued technology stocks that have suffered tremendous losses recently. Inflation and interest rate hikes initially weighted heaviest on unprofitable tech stocks, but we have since seen more established, profitable companies experience major declines. Netflix and Meta Platforms (Facebook), for example, have lost -71% and -52% so far this year.

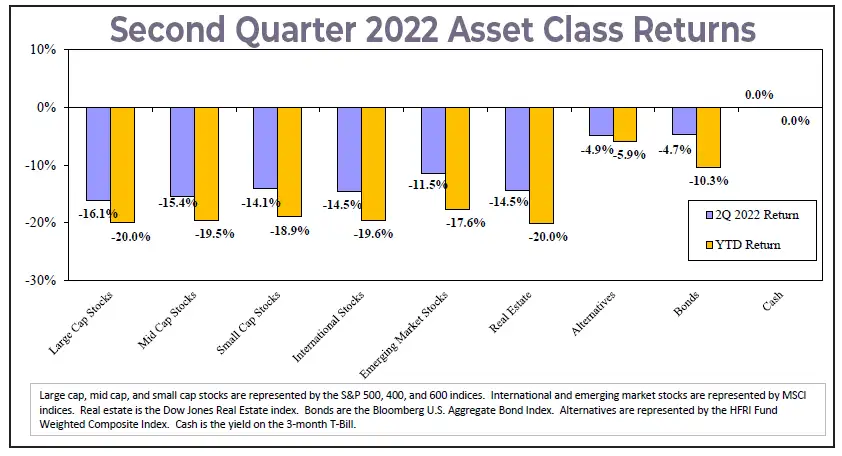

2nd Quarter 2022 Asset Class Returns

US DOLLAR STRENGTHENING

The US dollar has been unusually strong against foreign currencies, driven by a flight to safety in the face of global uncertainty and rising US Treasury yields that offer better returns to foreign investors. However, a strengthening dollar is a headwind for US investors owning international stocks. Despite this headwind, international stocks have slightly outperformed US stocks this year, despite significant economic troubles abroad. With the US dollar near historically high levels and valuations for international stocks far lower than US stocks, it would not be surprising to see international stocks outperform in the years to come. Thus, it remains important to maintain a proper allocation to international stocks for diversification and the likelihood of stronger returns.

RECESSION ON THE HORIZON?

Many analysts had previously forecasted a recession by the end of 2023, but recent economic developments suggest that one may come sooner. Real GDP in the US decreased by -1.6% in the first quarter. The definition of a recession is loosely defined as two consecutive quarters of negative GDP growth. Consensus estimates for the second quarter are mixed, with most analysts estimating real GDP growth ranging from either slow growth to further decline. Notably, the Federal Reserve Bank of Atlanta has projected a decline of -2.1% as of July 1st. Other data points also point towards troubling times. The yield curve between 10-year and 2-year Treasury bonds has inverted several times in recent months. An “inverted” yield curve where longer-dated bonds yield less than shorter-dated bonds has often been a predictor of coming recessions. Consumer sentiment is also at an all-time low.

With the probability of a recession increasing, 10-year Treasury yields have dipped from a high of 3.5% in mid-June to just below 3% at the end of the quarter. Nonetheless, rates still ended much higher than the 2.3% yield as of the beginning of the quarter, resulting in another tough quarter for bond returns since yields and prices move inversely to one another.

GOING FORWARD

MUnfortunately, there is no certainty of a quick stock market rebound from the downturn experienced in the first half of 2022. Rising inflation is likely to continue to elevate costs and weaken corporate earnings. The potential for higher interest rates will make it more difficult for firms to finance profitable projects. Valuations have declined, but the overall stock market remains richly priced relative to historical levels. While it has been a challenging environment, more defensive strategies have helped reduce downside risk, especially value and low volatility stocks. Short duration bonds have reduced the downside risk of rising interest rates. Alternative investments, most notably the funds used for managed futures and style premia strategies, have performed exceptionally well when diversification was needed the most.

Although expected returns and volatility remain uncertain in the near-term, we’ll manage through any further market weakness. These periods are uncomfortable, but they should not change the way you live your life. We would be happy to discuss your portfolio and our strategies for risk control any time if you have questions or start to get nervous.