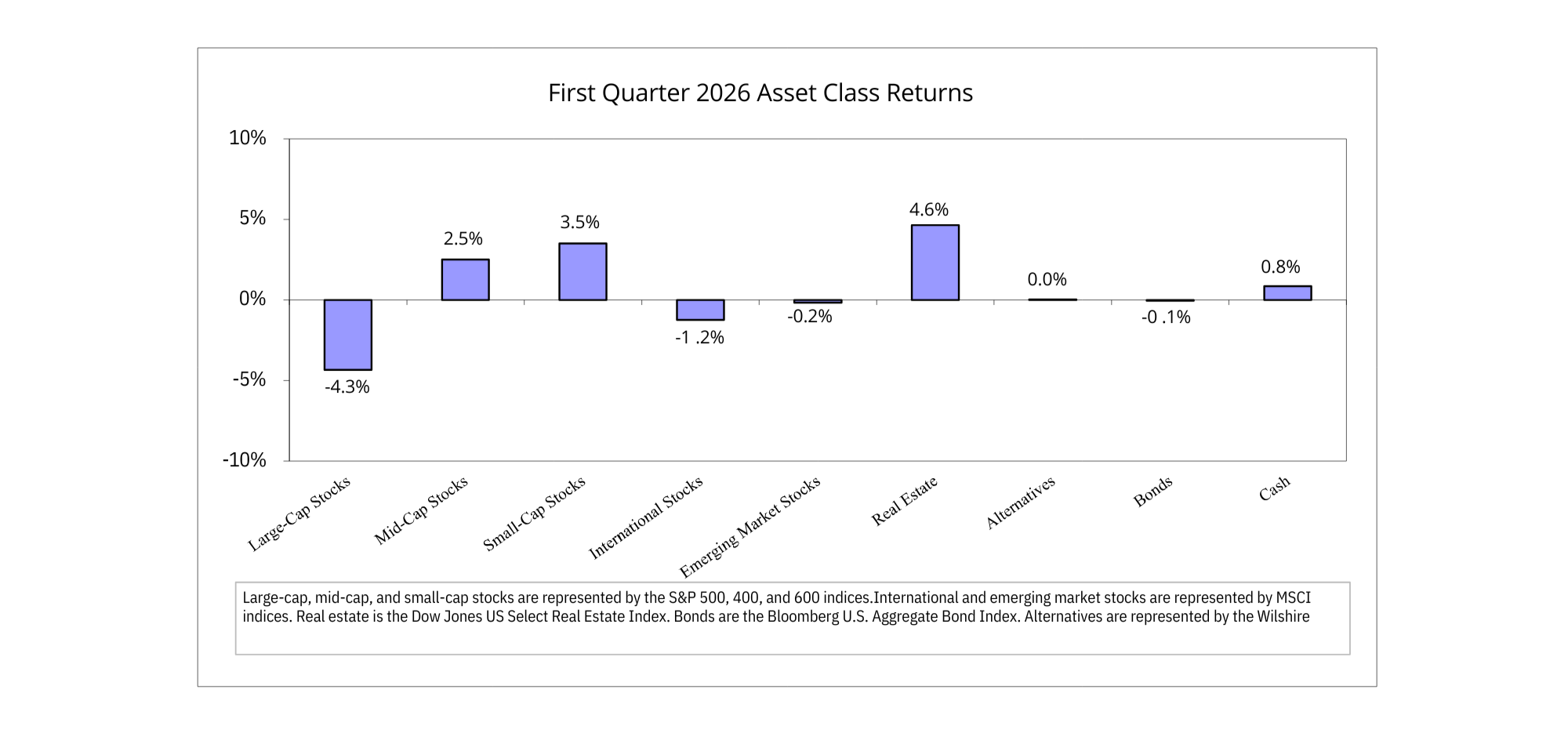

Throughout the last few weeks, headlines have been dominated by the United States’ military buildup in the Middle East. While this escalation has caused some fear from investors and negatively impacted some parts of the market, other parts have performed quite well, and the market overall has proven resilient. U.S. large-cap stocks were a drag on returns as the S&P 500 fell by 4.3% in the first quarter, while mid-cap and small-cap stocks were up 2.5% and 3.5%, respectively. International stocks were down slightly for the quarter. Rising bond yields because of higher inflation expectations put downward pressure on bond returns and ended the quarter flat.

Market Impact from the Iran War

U.S. airstrikes on Iran began on February 28, 2026, resulting in the deaths of Iran’s Ayatollah and several other high-ranking political and military officials. Retaliation measures ensued as Iran launched counterstrikes on neighboring countries and on oil tankers passing through the Strait of Hormuz, a crucial waterway through which 20% of global oil is transported. This disruption caused oil prices to skyrocket. Crude oil rose by about 50% from $67/barrel to over $100/barrel in just one month.

Accordingly, most stock sectors declined in March. The only outlier was the energy sector, which benefited from the elevated prices and was up over 10% during March and 37.9% for the first quarter. Technology stocks trailed the S&P 500, down 7.5%. The Magnificent 7 stocks that have dominated returns over the past three years fared even worse, dropping 12.1%. Given the recent rotation out of technology stocks and into sectors such as energy, materials, utilities, and consumer staples, it is no surprise that the value and low volatility factors significantly outperformed the market in the first quarter, whereas growth stocks struggled.

The rise in oil prices also affected the bond market, as increased concern about inflation from rising energy costs drove bond yields higher. The aggregate bond market was down 0.1% for the first quarter, while shorter-duration bonds performed slightly better. Fed officials were cautiously optimistic about gradually easing short-term interest rates at some point this year before the war broke out, but prolonged elevated fuel prices may cause them to change course.

Past conflicts in the Middle East (such as the Yom Kippur War in 1973 and the Iranian Revolution in 1979) contributed to stagflation, a combination of stagnant economic growth, high unemployment, and high inflation. However, there were other issues, primarily policy mistakes, during the 1970s that were likely larger causes of that era’s notorious economic environment. Today, the U.S. is much less dependent on oil imports than it was in the 1970s. The U.S. economy is also less sensitive to shocks in oil prices. Aided by increased fuel efficiency and a shift to a more service-based economy, oil consumption has remained relatively flat since the 1970s, while the economy has tripled in size, which translates to oil intensity declining by over 70% since the 1970s. While a prolonged conflict may certainly cause greater economic hardships and rattle markets, it is possible that the impact may not be as severe as it has been in the past.

It is also important to note that the stock market has historically risen during periods of military action. This may seem counterintuitive since the market hates uncertainty. But the data bears this out. We did a study on stock market returns during times of war several years ago. It was picked up by Barron’s and other national publications. It showed that stocks have generated an additional almost 1.5% extra return during military conflicts and, importantly, did so with less risk. This was true for both large-cap and small-cap stocks. Bonds, on the other hand, have generally underperformed during periods of war, likely due to higher inflation.

Gold’s Roller Coaster Quarter

The sharp rise and subsequent fall in gold prices were also notable events in the first quarter. Coming off a year where the price of gold rose by over 60%, gold continued its meteoric rise, gaining 22% in the first two months of the year. The precious metal then fell by over 11% in March. Over the long term, gold has generated a level of returns similar to bonds while exhibiting volatility greater than stocks. The asset also has an inconsistent history as an inflation hedge (gold prices dropped by over 10% while inflation peaked in 2022). While gold may have its place in some portfolios, it has an erratic return history. Indeed, it has not been much of a safe haven lately.

Rather than using gold as a hedge against uncertainty, we prefer our portfolio of liquid alternative investments. It has been quite successful in providing returns much higher than traditional bonds while reducing volatility. Strong returns for alternatives continued into this quarter, with all strategies in the portfolio posting positive returns. The managed futures and style premia funds led returns, each posting gains of over 9%.

Staying the Course

Despite the recent geopolitical noise, the market downside has been quite limited thus far. The S&P 500 has yet to enter correction territory (a 10% drop from its peak). Volatility may persist, but it is not uncommon for stocks, and it is not an indication of what future returns will look like. The past three years, the S&P 500 experienced intra-year drawdowns of 10.3%, 8.5%, and 18.9%. The total return of the index during those last three calendar years amounted to 26.3%, 25.0%, and 17.9%. Staying invested during the highs and lows almost always works better than attempting to time the market.

To learn more about Armbruster Capital or to speak with one of our registered investment advisors, call # (585) 381-4180 or contact us through our website.

Disclaimer: Armbruster Capital Management’s views as portrayed in this post are subject to change based on market conditions and other factors. These views should not be construed as a recommendation for any specific security or sector. Investing involves risks, and the value of your investment will fluctuate over time, and you may gain or lose money. Past performance is no guarantee of future results.