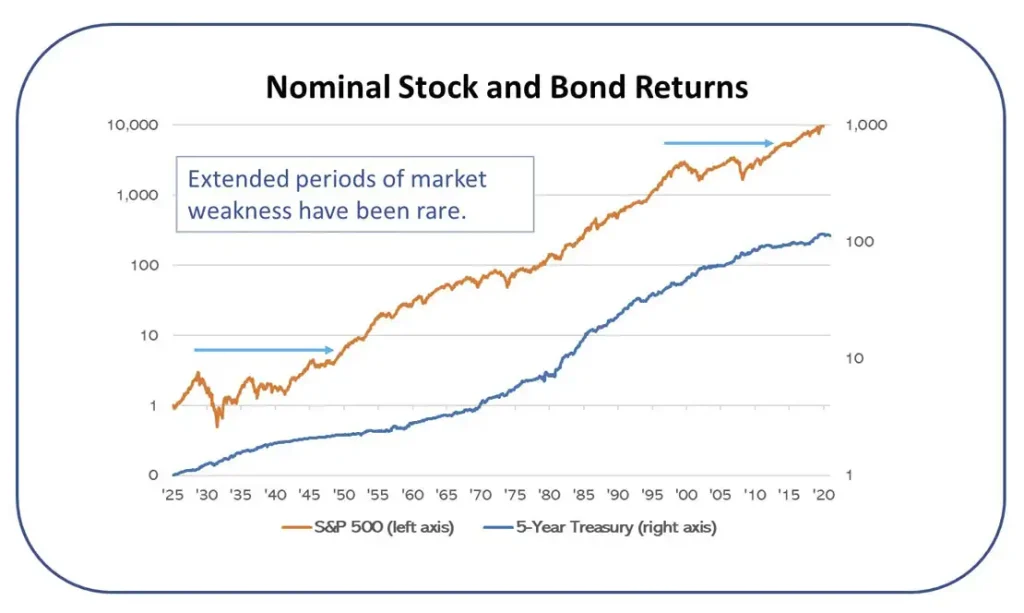

It is well known that the stock and bond markets have generally gone up over time. Why else would anyone invest? Sure, there have been a few “speed bumps,” such as the Great Depression and the decade of 2000 when things didn’t work out so well (see nominal return graph), but generally investors have made money by being invested. But what happens when you factor in inflation?

1925-2022 Nominal Stock and Bond Returns

US Inflation has averaged less than 3% annually over the past hundred years. Stocks and bonds have generated average compounded returns of almost 10.5% and 5.1%, respectively. Clearly, over time, inflation has been no match for the compounding of good investments. The problem is that this is true over time, but not all the time.

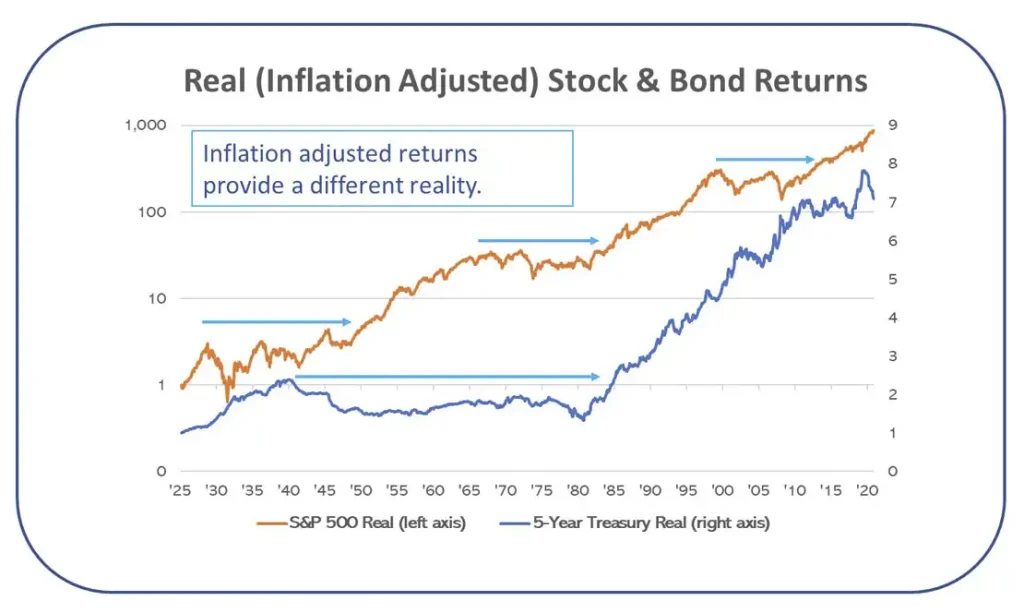

If we look at the same graph but subtract inflation from the returns of stocks and bonds, to get at their real returns, it paints a different picture (see real return graph). There is a 20-year period from roughly 1960 to 1980 where stocks earned no real return. They kept up with inflation, but investors would have taken a lot of risk just to maintain their purchasing power. Unfortunately, that was the good news. Bonds earned no real return from around 1940 to 1985, a 45-year period. Imagine saving and investing your whole life and being no better off for it after four decades.

1925-2022 Real (Inflation Adjusted) Stock and Bond Returns

Could something similar happen today? Is it happening already? Inflation certainly has picked up lately after many years of being fairly moderate. The Fed initially told us this inflation was “transitory” as the economy reopened after Covid and supply chains were disrupted. However, they are no longer using that word, and the threat of persistently high inflation seems to be increasing.

There are indications inflation could continue, such as supply chain issues that don’t seem to have a quick fix, the continuation of easy money policies by the Fed, and a desire to pump more fiscal stimulus into the economy by our ruling party. However, there are also reasons to hope inflation could subside. Some are optimistic, such as what appears to be increased fiscal responsibility from some quarters and a more hawkish tone from the Fed. But some are decidedly gloomier, such as an unprecedented debt overhang that threatens economic growth.

Just like trying to time the stock market, there is no good way to know for sure what will happen with inflation and the broader economy. There’s an old joke that God created economists to make weather forecasters look good. So, while inflation is a concern, it isn’t a foregone conclusion that we’ll repeat the high inflation or even stagflation of the 1970s.

Still, even temporary inflation can be damaging for investors and savers. It is unlikely that the increases in inflation will reverse, as deflation is quite rare, so prices may be permanently set higher in some areas. That means sitting on large amounts of cash is counterproductive. It also means that bond returns, even if positive, will be negative in inflation-adjusted terms. Stocks will likely at least break even over longer time periods.

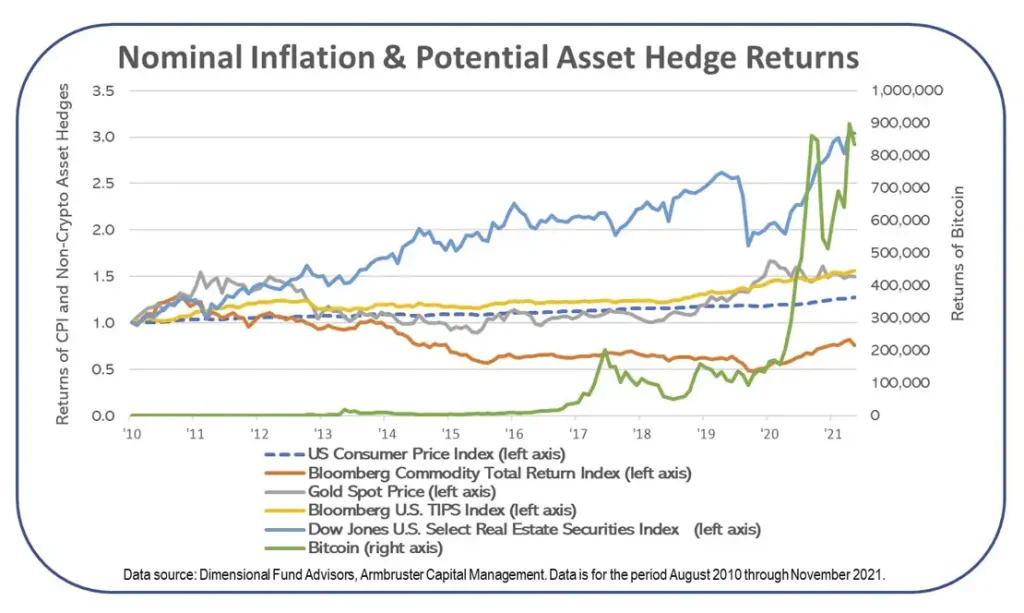

There are other asset classes that investors can consider to address inflation, and undoubtedly, you’ve heard about them lately in the news or from the financial media. Commodities, gold, TIPS, real estate, and even cryptocurrencies are cited as inflation hedges. Many of these assets have inflation hedging characteristics, but none is a true inflation hedge. In fact, many of them have gone down in value or held steady as inflation has heated up, see the recent performance of gold and Bitcoin as examples.

Inflation vs. Potential Hedge Asset Class Returns

Diversifying into alternative asset classes and away from bonds isn’t necessarily a bad idea, and in fact we have done just that for many years in an attempt to address historically low interest rates. However, reacting to inflation that may or may not be a longer-term problem seems rash, particularly when the solutions are imperfect at best.

So, for now we’re sticking with our long-term approach of stocks for growth, high quality and short-duration bonds for safety and liquidity, and some alternative investments to help control the risk of stocks while reaching for a little better return than bonds. It sometimes seems quaint to hold the line and diversify, but long-term empirical data suggests that is the best approach.

Watch the related ACM InvestED Vidcast: Investing during inflation: Protect your returns when investing in a high inflation environment