Index investing was much in the news in 2017. An article in the Wall Street Journal in late November noted that U.S. index funds have seen cash inflows of around $1.7 trillion since 2009, compared with outflows of nearly $1 trillion for actively-managed mutual funds. Another article noted that investors had collectively invested $436.5 billion this year into index funds globally through December 20, according to EPFR Global.

Clearly a lot of investors are waking up to index funds, which attempt to mimic the returns and risk profile of a particular market, rather than trying to “beat the market” as actively-managed funds do.

That said, index funds have been derided as unamerican and Marxist. They have been accused of settling for average and overweighting overvalued stocks.

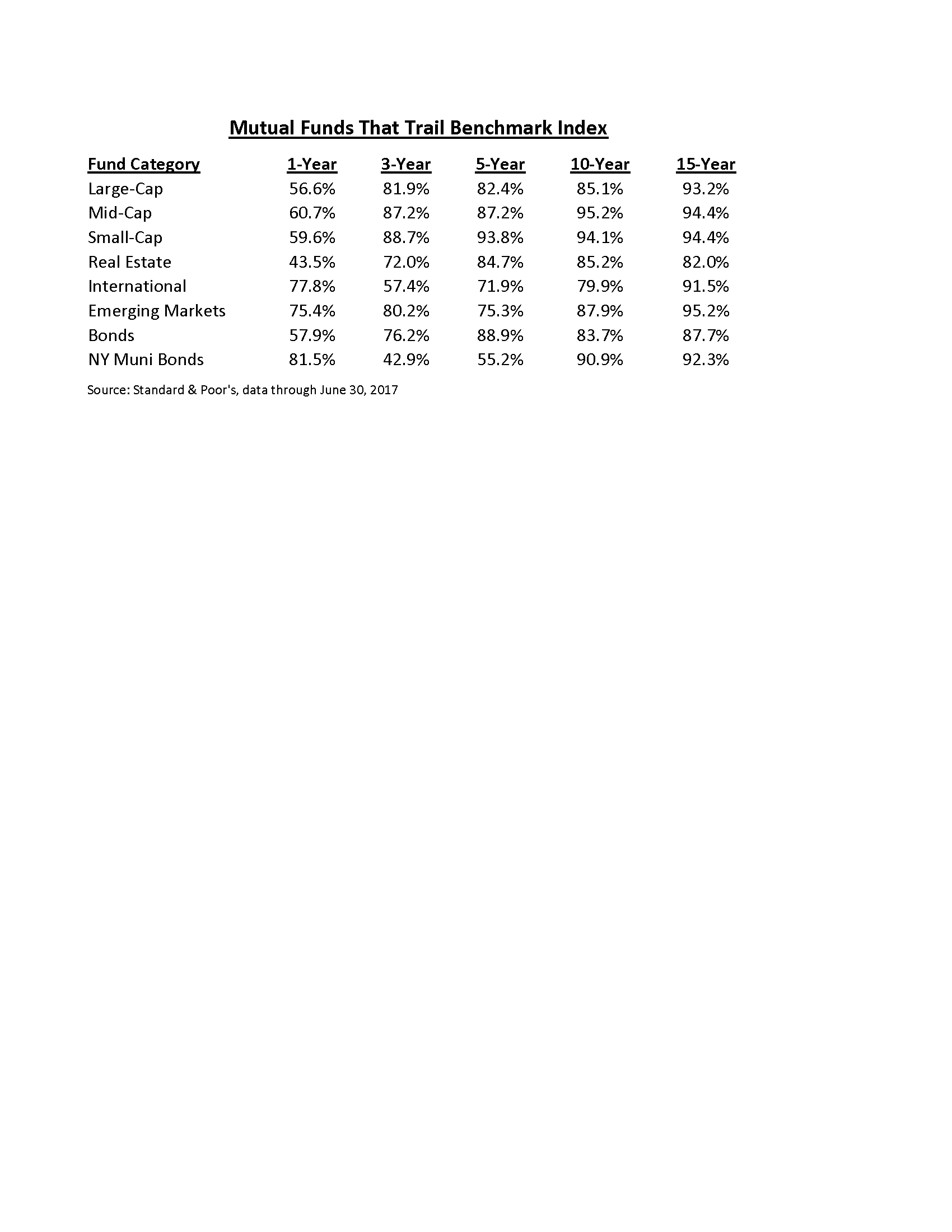

Yet, despite the criticism, index funds have hugely outperformed actively-managed funds in recent years. There is actually evidence dating back almost 100 years that index funds outperform active funds in just about every market environment. However, the past couple years have seen index funds truly dominate. A semiannual study from S&P (see nearby chart) shows the percentage of actively-managed funds that underperform their benchmark index. The news has not been good.

Over a one-year period, most actively-managed funds underperform, but many still beat their benchmarks. However, over time, as their higher fees compound, the vast majority of actively-managed funds trail the market. You can see from the data above that in most asset classes, over 90% of actively-managed funds fail to beat their benchmarks over 15-year holding periods.

Yet, actively-managed funds charge higher fees, as they claim their superior performance justifies higher costs. In fact, it is these high fees that weigh on returns and make their performance so poor.

Index funds have outperformed for decades, with a fraction of the cost of active management. Still, most investors still utilize actively-managed funds. We have read studies claiming that indexing accounts for 20% of the overall stock market, but others suggest that number is as high as 35%. In either case, indexing is still squarely in the minority.

Critics claim that as indexing grows to be too large a part of the stock market, it could make investing less efficient. We agree, but the level at which that will occur is likely closer to 90% of the market. As long as there are active traders determining the prices of stocks and bonds, index investors can passively reap the rewards of the market in a low-cost, tax-efficient manner.

Interestingly, ultra-low-cost index funds became even cheaper to own and trade during 2017. Expense ratios for index funds and indexed exchange-traded funds (ETFs) offered by Vanguard, Charles Schwab, Fidelity, and others all fell during the year. While the average cost to hold an actively-managed mutual fund is around 1.0%, it is possible to own an index fund that invests in the entire U.S. stock market for 0.03%.

However, not all index funds are created equal. While it is possible to buy a fund that tracks the market for an annual cost of 0.03%, other S&P 500 index funds have expense ratios ten times as high, and some even charge up front sales loads of 5.75%. Also, most large index funds and ETFs are very tax efficient, but not always. The S&P 500 fund index fund offered by PNC Bank paid a capital gains distribution of over 20% last year. Many investors will have to pay tax on that gain, even if they don’t sell their shares. By comparison, Vanguard paid no capital gains distributions on its S&P 500 fund. We don’t want to be overly dramatic, but an index fund paying out a 20% capital gain should be punished by a long, slow, horrible death.

Trading commissions also declined during 2017. Our primary custodians, TD Ameritrade and Charles Schwab both reduced commissions on stock and ETF trades. However, many of the ETFs we use trade without any commission at all. This makes it all the more cost effective to use index strategies. And, remember, what you don’t pay out to financial intermediaries stays in your account to grow and compound over time.

To Download the complete 2017 Q4 Newsletter please click below.